¿Qué podemos esperar del mercado esta semana? 140 para tratar las cuatro áreas clave para tus finanzas y la economía global más un «Y si…»

![]()

Macro

Dollar, deficits and shale – On Monday the New York Fed president raised the forgotten subject of America’s trade balance. At 3 per cent the deficit is half the worst levels of 2006. One source of improvement is the shale bonanza. But a smaller petroleum goods shortfall hides the fact that the non-petroleum goods deficit is approaching 2006 levels again. A second helping hand has been the dollar, which is a tenth weaker in real trade-weighted terms versus 2006. How damaging could this dollar rally be now? The last two dollar up-cycles in the early 1980s and late 1990s coincided with the deficit widening by 3 to 4 percentage points of output. But back then oil deficits were large and a rising dollar was tempered by falling oil prices. As energy independence approaches the US trade deficit may become more sensitive to currency swings.

Strategy

US shopping – «Germans on US Buying Binge!» screamed the financial press this week. Supervisory boards apparently think America is a better bet than Europe and want to spend euros while they are still worth something. Evidence? Certainly not that eurozone companies were themselves targets for a record 40 per cent of outbound US acquisitions last year – that doesn’t fit the story. Nor does the fact that America has been the top German shopping destination for the last five years and indeed for 14 of the last twenty. Sure $65bn of US deals has been announced since January, more than in any full year in two decades. But this represents just 17 per cent of overseas deals by volume – barely higher than last year. Indeed 30 more transactions are required just to reach Germany’s twenty year average of 83 American acquisitions every year.

Stocks

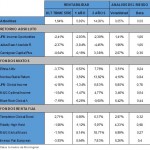

Expensive defensives – Nerve wracking isn’t it? The largest bets in your European equity portfolio are defensive sectors such as healthcare and food and beverage. They are also the most expensive. The former is a third dearer than the market based on forward earnings and a fifth above its own ten year history. But they keep outperforming. You keep buying. Surely this ends badly! Maybe not if you reckon a soggy and disinflationary Europe reminds you of Japan. From the summer of 1996 until two years ago the Topix index drifted southward save for a brief dot.com wind. Pharmaceuticals and food were the first and sixth best performing sectors over this period. Chemicals – which includes the likes of Shiseido and Kao – was next. They simply got more and more expensive. Indeed the latter’s relative earnings multiple only fell twice over those 16 years.

Finance

Active ETFs – As the PIMCO story thrusts active ETFs into the spotlight this week some perspective is required. First, active ETFs are too small to pose any systemic risk. Total assets in all US active ETFs amount to a trivial $15bn – that is just 1 per cent of America’s total ETF industry or 0.1 per cent of US mutual fund assets under management. Indeed, the two largest active ETFs – both managed by PIMCO – account for nearly half of all the money in this nascent asset class. But might active ETFs catch on? For passive ETF providers moving up the value chain must be tempting – although endorsing active management surely contradicts their philosophical distrust of stock picking. Meanwhile traditional money managers offering cheaper active products risk cannibalisation. Ultimately success may depend on whether investors are fleeing active funds due to price or performance.

Digestif

Mansion tax – Labour will introduce a mansion tax on UK properties worth over £2m if it wins the election. Leaving aside «poor» landlords with 20 flats worth £100,000 each, how punitive is this for «rich» homeowners? Consider a household making £120,000 a year. It takes 14 years to accumulate a £500,000 deposit for a £2m home, assuming a 40 per cent tax rate and putting aside half of net earnings. The mortgage is interest-only. On top of £100,000 in stamp duty, £677,000 has already been paid in income taxes. Six more years saving to afford a £200,000 renovation equals another £270,000 in income taxes, not to mention £40,000 in VAT. Happily, the house is now worth, say, £2.5m. Sadly, a mansion tax costs another £5,000. That adds up to £1m in taxes for £1m of equity – a 100 per cent wealth tax!

Publicaciones relacionadas:

Tres activos refugio para superar la tormenta financiera

Tres activos refugio para superar la tormenta financiera

Bankinter y Sabadell luchan por recuperar las posiciones perdidas en Bolsa

Bankinter y Sabadell luchan por recuperar las posiciones perdidas en Bolsa

Los 22 fantásticos de la Renta Variable española

Los 22 fantásticos de la Renta Variable española

¡Alerta Fibonacci! Peligro en los mercados para el 22 de enero

¡Alerta Fibonacci! Peligro en los mercados para el 22 de enero

El café vale casi la mitad que hace un año ¿usted lo ha notado?

El café vale casi la mitad que hace un año ¿usted lo ha notado?

Barcelona Trading Point, cita ineludible con el mundo bursátil

Barcelona Trading Point, cita ineludible con el mundo bursátil

La semana en los mercados (del 22 al 26 de septiembre)

La semana en los mercados (del 22 al 26 de septiembre)

Bolsa y políticos no se llevan bien

Bolsa y políticos no se llevan bien

Trimestre negro en los mercados… ¿se ha salvado alguna inversión de las pérdidas? Y tú, ¿cuánto has perdido?

Trimestre negro en los mercados… ¿se ha salvado alguna inversión de las pérdidas? Y tú, ¿cuánto has perdido?

El trading en línea con FXGM

El trading en línea con FXGM

Las comisiones por invertir en bolsa

Las comisiones por invertir en bolsa

Diferencias entre gestión activa y gestión pasiva de las inversiones

Valores en los que conviene fijarse

Encontrando oportunidades en un mercado volátil

¿Es posible invertir sin riesgo? Trece valores para apostar sobre seguro

Diferencias entre gestión activa y gestión pasiva de las inversiones

Valores en los que conviene fijarse

Encontrando oportunidades en un mercado volátil

¿Es posible invertir sin riesgo? Trece valores para apostar sobre seguro

¿En qué se parecen los fondos de inversión y el fútbol?

¿En qué se parecen los fondos de inversión y el fútbol?